Bon4equi Global Consulting Private Limited, B-4076, Oberai garden Chandiwali, Andheri (E), Mumbai -400072

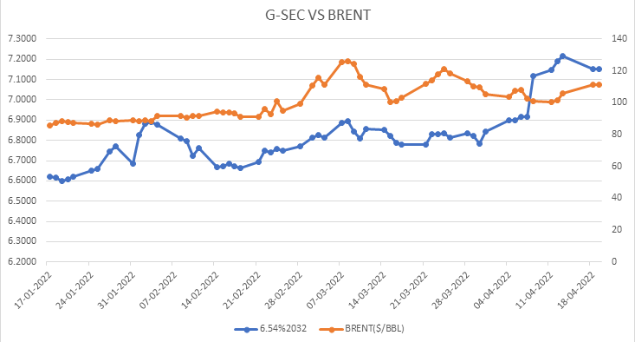

The trend in energy prices and Treasury bond yields can be used as an indicator of a country’s economic outlook. As adverted above, an optimistic economy is favourable to rising bond yields. Similarly, when the economic growth prospects are optimistic, and the demand for crude oil is optimistic, it will drive rising crude oil prices. Therefore, the price relationship between the two is affected by the economic cycle and positive correlation.

Inflation expectations also have an impact on crude oil prices. Past price trends have shown that the year-on-year growth rate of oil prices is positively correlated with the India’s CPI (inflation) growth. Therefore, the rise in crude oil prices itself boosts inflation expectations, thereby increasing nominal bond yields and affecting bond prices. Therefore, since the beginning of this year, oil prices and inflation have often been mentioned in the same breath due to their correlation. In addition, the strong rebound in oil prices before March was also accompanied by rising bond yields.

Of course, in addition to Oil price affects the entire economy, especially because of its use in transportation of goods and services. A rise in oil price leads to an increase in prices of all goods and services. It also affects us all directly as petrol and diesel prices rise. As a result, inflation rises. A high inflation is bad for an economy. It also affects companies - directly because of a rise in input costs and indirectly through a fall in consumer demand.

This is why the rise in global crude prices comes as a bane to India. Every $10 per barrel rise in crude oil price helps increase retail inflation by 0.2% and wholesale price inflation by 0.5% and Bond yield increases with inflation.

In last monetary policy (6th to 8th April 2022) the inflation is projected at 5.7% in 2022-23, with Q1 at 6.3%, Q2 at 5.8%, Q3 at 5.4%, Q4 at 5.1% with assumption of normal monsoon in 2022 and average crude price of US$ 100 per barrel.

Bon4equi Global Consulting Private Limited, B-4076, Oberai garden Chandiwali, Andheri (E), Mumbai -400072

Investment In Bonds is #1 online Market place offering largest collection of bonds and NCDs for multiple Investment choices.

©2022- Investmentinbonds.com All Rights Reserved.

We provide financial planning, advice and resources that investors need. As the financial industry evolves and customer needs become more complex, we have and continue to reinvent, innovate and transform ourselves to be ready for the financial landscape of tomorrow.

Our team is led by Bhavanand Kumar Mishra who has outstanding expertise in the Bond Market, Forex. He is M.B.A, certified associate of Indian Institute of Bankers, certified treasury professional holder from IIBF, Mumbai. He has worked as Chief Dealer in almost all asset classes especially in the Fixed Income in the treasury, with twenty plus years of expertise including overseas experience at London & Birmingham in U.K. in the Punjab National Bank, which is the second largest PSU Bank in India. Mr. Mishra is supported by a team of young professionals.

The size of Indian Bond market is increasing substantially year on year basis and so the opportunity also multiplies. Indian Bond market consists of Central Government securities (G-Secs), State Development Loans (SDLs), Treasury Bills, these securities are also called as Sovereign assets classes. Particularly State Development Loans is a higher yield asset class and suitable for the retail investors. State Development Loans (SDLs) maintains 25 to 50 bps spread from the G-Secs in the respective maturities however, these spread is not sacrosanct and may vary depends on the multiple variables.

As far as Corporate Bonds are concerned, Public Sector Undertakings like PFC, REC, NABARD, NHAI, etc, Private Companies, NBFC are issuing multiple bonds round the year having different maturities. These corporate bonds carry substantial spread from the G-Sec.

Generally, before investing in Bank/Corporate Fixed Deposit, depositors compares the rate of different bank's offered rate of interest and then decides where to invest in. Generally, investors don't give importance to the fact that their deposits per bank is secured only up to INR 5 Lakh. Further, if the individual left with additional surplus money, he/she chooses to invest in the Debt MFs. In the debt MFs, there are multiple entry or/and exit load and other charges which makes their return less profitable than their direct investment in the bond. At the end of day, Fund Managers of the Debt MFs invest in the bonds only which are available in the market.

Summary - The diversification of the investment portfolio is the key to manage hard earned savings. While we don't negate the importance of Bank's Fixed Deposit, but at the same time we also don't appreciate investing all the money either in the Bank/Corporate FDs or in the MFs. In the modern era, when all the information are widely and easily available, we must change the investing habits a little bit to earn more without putting any extra effort. Interestingly, investing in the bond is quite easier than our believe as everything can be done sitting at the home.

Bonds are issued by organizations generally for a period of more than one year to raise money by borrowing. Following are the types of bonds:

In general, Bonds and Debentures are interchangeably used in conversation but they have their own definition and characteristics related to them.

Here is the list of popular Bonds and Debentures available in India.